If you are interested in technology, blockchain or cryptocurrency it is most likely that you have encountered the term "Internet of Value". The Internet of Value (IoV) is a concept proposed by Ripple which envisions an internet where value is transferred as easily, cheaply and reliably as data is transferred now. Blockchain technology supports this vision by facilitating access to value transfer infrastructure.

Read on to find out more about the concept and its implications for the world of finance.

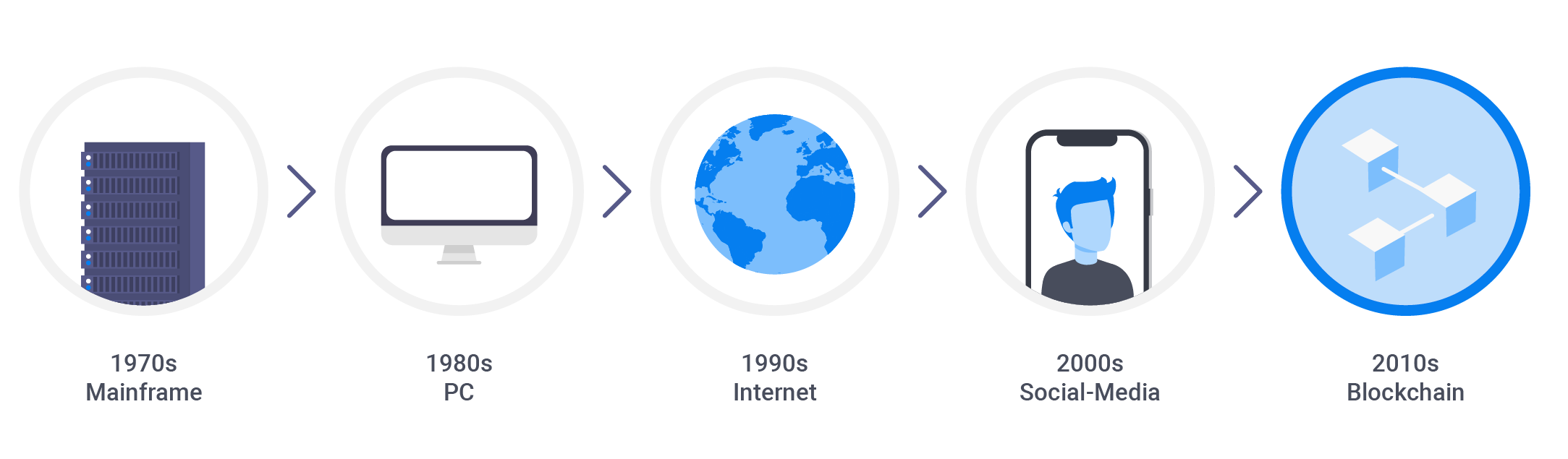

From mainframes to blockchain.

In the past 4 decades, we witnessed the move from simple mainframes to PCs, to the Internet, Social media and now to Blockchain. We have seen the evolution of smartphones, drones, AI, Cloud, online streaming, electric and self-driving vehicles, and finally blockchain technology and digital assets.

After the financial collapse of the late 2010’s, people were looking for alternatives. The banking system had apparent flaws rooted in centralization and it was time for a change. In 2008, the Bitcoin whitepaper was published by a person or group called Satoshi Nakamoto. Bitcoin was described as a Peer-to-Peer electronic cash system. This marked the start of a slow revolution with the goal of open and decentralized (digital) assets for all, with built in transparency and security.

After Bitcoin, other digital assets were created, some using new and unique blockchain accounting systems. Ripple and XRP were among the early alternatives to Bitcoin. The XRP Ledger creators saw flaws in the Bitcoin system, so they decided to build a different model. They wanted to address the issues that a Proof-of-Work (PoW) system is susceptible to. Namely scalability, the threat of a 51% attack (malicious centralization) and the ever more apparent environmental strain of mining.

In 2011, Arthur Britto, Jed McCaleb, and David Schwartz started work on what is now known as the XRP Ledger. In 2012 Chris Larsen joined the team and they founded OpenCoin, which was later renamed to Ripple Labs, Inc. The beginnings of the tech can be traced all the way back to 2004 and a developer named Ryan Fuger, who created a payment protocol and decentralised platform called Ripplepay.

What is the Internet of Value?

The Internet of Value, described in simple terms, is an online space where people can instantly transfer value between each other, eliminating the need for the middlemen and most costs. Theoretically, anything of monetary or social value can be transferred between parties, including currency, assets, stocks, securities, intellectual property rights, scientific discoveries, and even a vote in an election.

Transferring value is already supported by legacy financial rails like SWIFT, blockchain like Bitcoin or Ethereum and new and emerging technologies or solutions like Interledger (ILP), PayID and many, many apps that make transferring value easier with existing infrastructure. All of these need to be connected somehow to achieve the vision and there are likely still a lot of unknowns.

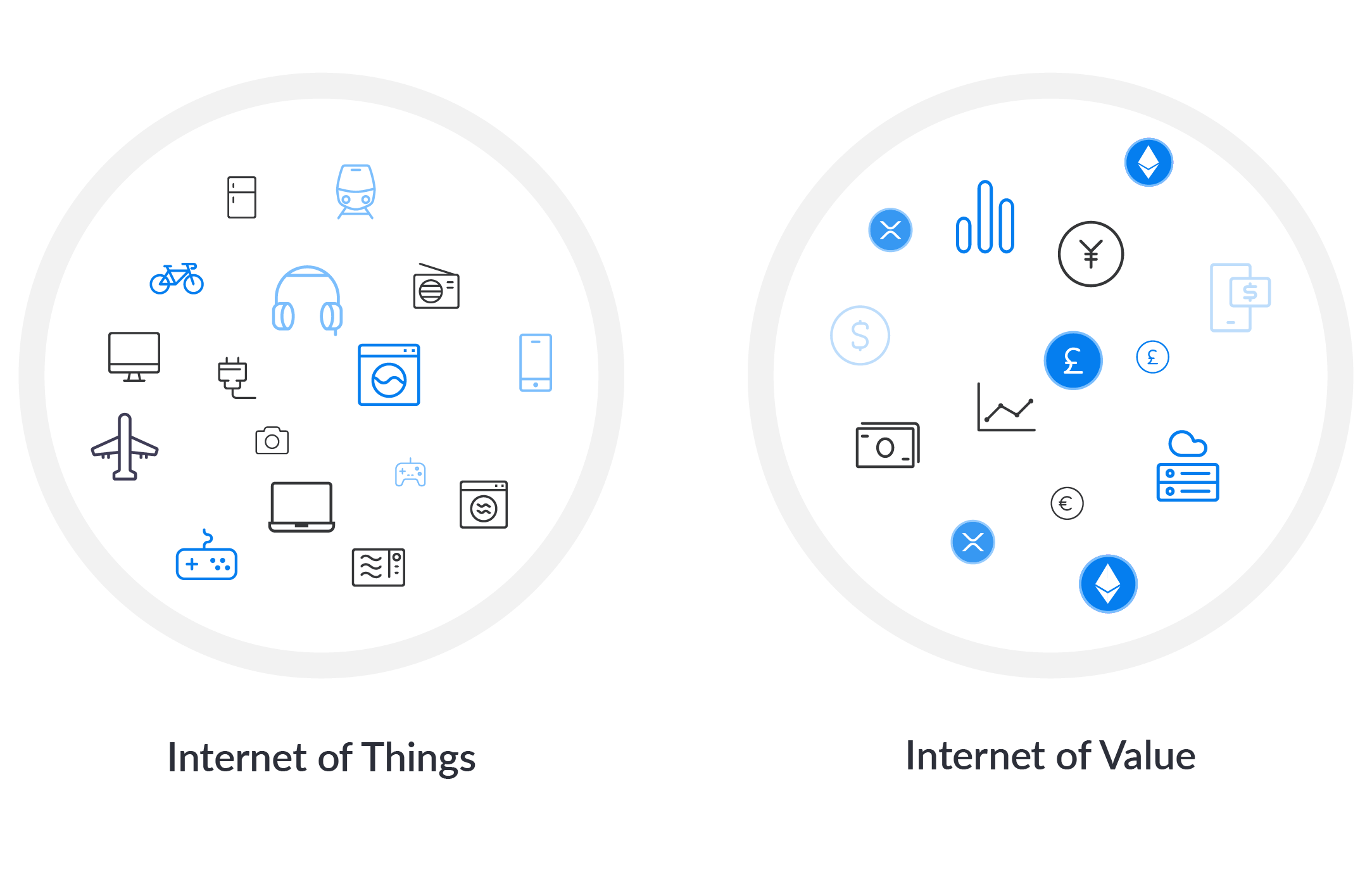

The Internet of Value sounds similar to the Internet of Things (IoT), which is a different concept but they do not necessarily exclude each other. On the Internet of Things any device can communicate with other devices, which forms a complex network that can produce more diverse results than human-human or human-computer interaction. IoT is interesting in this respect as the devices in this network might potentially want to exchange value too and that is why these two will likely evolve in parallel.

What problems does the Internet of Value solve?

Moving money is expensive, especially when it comes to cross-border payments and cross-system transfers. It is also slow in the case of settlement. End-users have become used to instant availability of information and are becoming increasingly used to instant access to their money too. This is a result of tech like cards and newer financial apps that make moving money more convenient and cheap.

The digital revolution of data has not been reflected as much in money and payments. Digital assets appear to be our best bet to achieve the goal of the Internet of Value. In different forms and with different underlying tech, digital assets like Bitcoin, XRP and potentially one day digital FIATs, promise us a world where value can be transferred reliably and instantly.

Another problem that the Internet of Value is trying to solve is the lack of access to financial instruments across the globe. The Internet is projected to surpass bank coverage globally with 1.7 B adults still underbanked and 4.1 B of the world population connected to the internet. Access to the internet means access to finance in the vision of the Internet of Value.

The last problem we will expose in this blog is the issue of transparency and accountability of current closed financial systems. With blockchain all transactions are public and immutable which cannot be said for most legacy rails. Stricter regulation is paving the way for new technology to gain momentum in the mainstream where users need more certainty and easier management of their money. With blockchain the possibility of actually owning your money is closer to coming true.