Digital banking is reshaping traditional financial services, making them faster, easier, cheaper, and more accessible.

Trends in digital transformation and changes in customer expectations have led banks to transform their businesses to remain relevant. New competition from FinTechs, digital banks, and mobile-only banks has given traditional banks new challenges. Although conventional banks offer the same services as digital banks, some key differentiators between the two make one more attractive than the other. FinTech empowers consumers to take responsibility for their financial decisions, leading to far more significant financial literacy than ever before. In short, FinTech combines traditional financial services with the latest digital technology and Big Data products, making life easier for customers.

It was not until the second half of 2010 that banks started to realize the emerging threat of FinTech companies. As FinTech start-ups are increasingly launching, e.g. N26 (2013), Revolut (2014), Monzo (2015 ), etc., fear of losing customers and market share has risen among banking institutions. This is increasing the growth of banking innovation teams to fight FinTech through investments, partnerships, and acquisitions.

But the vital question remains. How are digital banks going to affect traditional brick-and-mortar banks? Will the customers leave their existing banks and switch to all digital services?

Two-thirds of banking customers say they plan to convert fully to a digital bank in the future.

(

Finder, 2020).

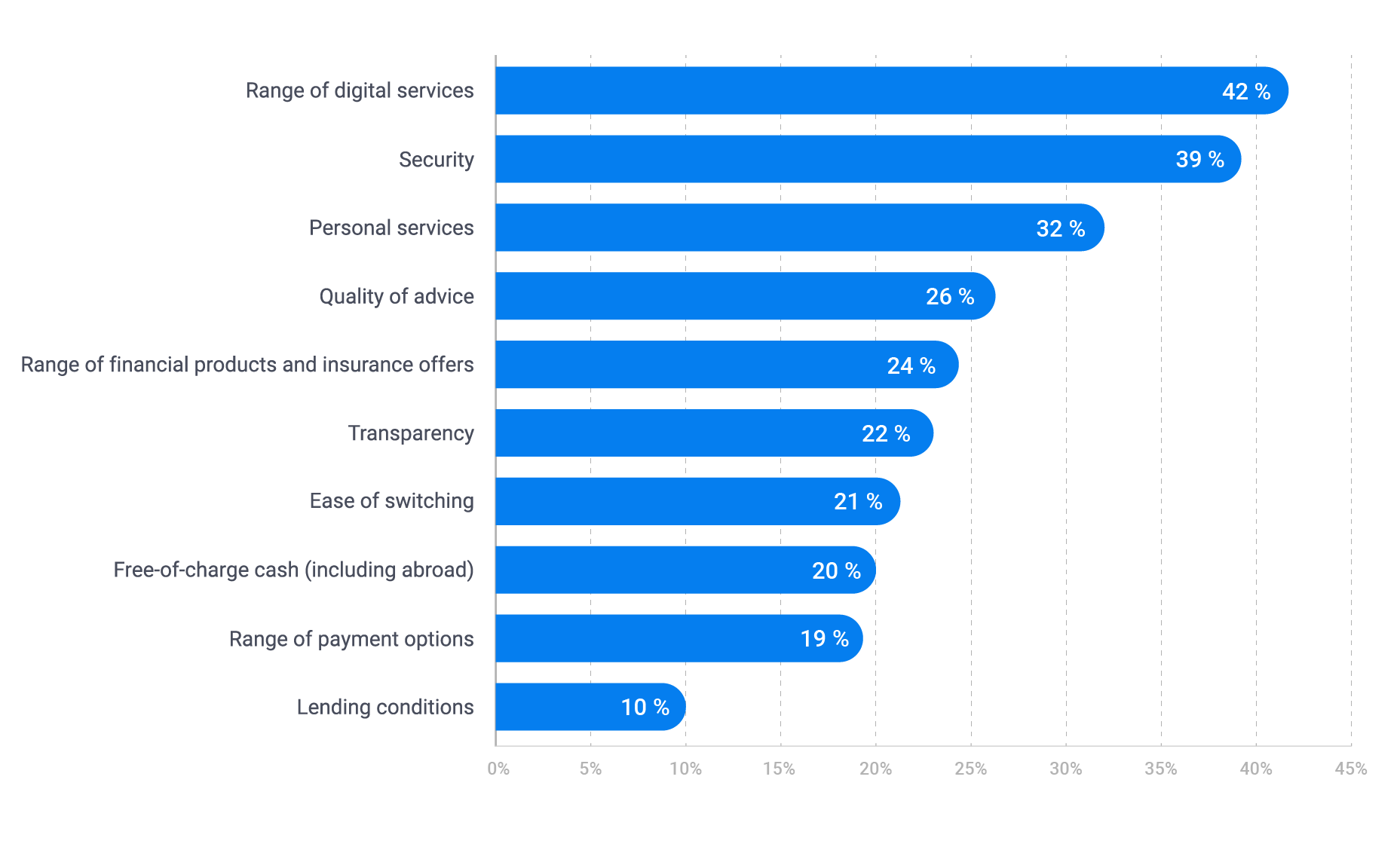

The reason behind it may lie in one of the many advantages of digital banking such as business efficiency, cost savings, increased accuracy, greater agility, enhanced security, and improved competitiveness. As you can see from the graph provided below the main benefits users find important are the range of digital services with 42%, security with 39%, and personal services with 32%.

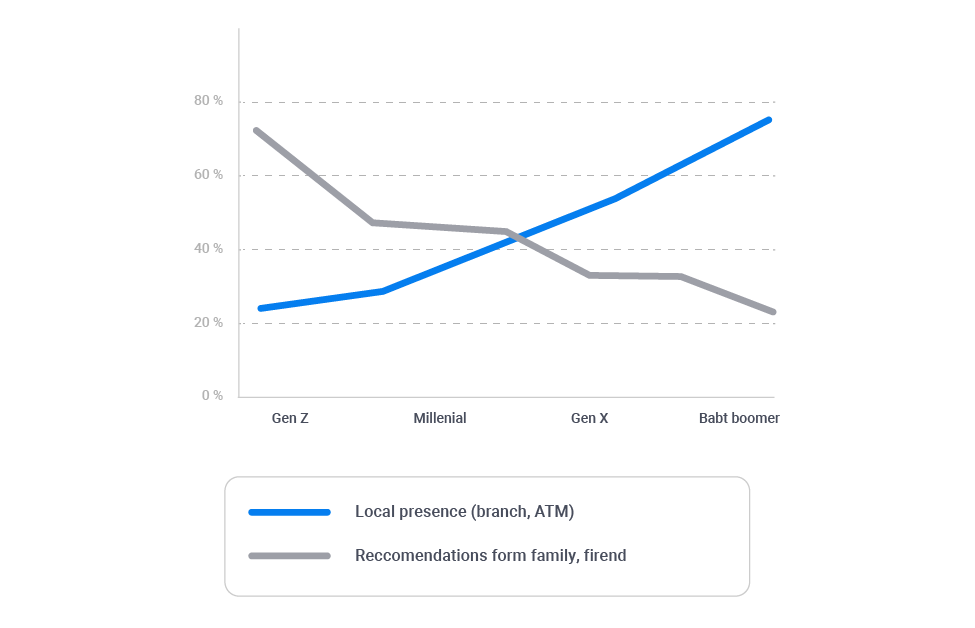

The most crucial factor that helped FinTech become a disruptive force in the financial world is the millennial population. Millennials are very demanding and less loyal as they expect personalized products and services according to their needs. They usually search for information, financial products, and tips online instead of following the traditional ways of finding information. How do other generations pick their primary bank account? You can see from the picture below that for example Gen Z generation considers recommendations from friends and family much more important than the local presence of the bank.

Despite all the benefits of bank digitization, traditional banking seem to continue playing a major role, because:

- Relatively simpler transactions have migrated to digital channels, but traditional banks are still important for more complex operations.

- Strict know-your-customer(KYC) and anti-money laundering policies.

- Many customers prefer personalized product advice.

- Most people prefer visiting a branch to open a new account, to learn about their budget, understand retirement options, and discuss and apply for a mortgage.

- Some financial products still require face-to-face interaction and physical signatures.

- Traditional banks provide a sense of continuity and security that digital banks find it difficult to reconcile.

In this FinTech era, financial institutions need to adapt to digital trends as soon as possible and better pinpoint the unmet digital customer needs. The growing expectation of financial institutions is to shift from product-based to customer-based models to equip themselves to offer fast, easy-to-use, personalized products and services to digital customers through the customer priority channel. By finding the right mix of acquisitions, partnerships, and investments, traditional banks are leveraging innovative solutions to address the emerging needs of their customers in this first era of digital financial services. According to CNBC, some of the largest US banks are increasing their investments in their potential competitors. The same goes for EU banks, as stated by Fintech Futures, where banks form strategic partnerships with start-ups to use their mechanism. The aforementioned will also open the door for banks to acquire exclusive rights to advanced technology that can provide a competitive edge over others, rapid expansion into new markets, and even a new customer base.